I recently posted the discussion I had with John Black, CEO of Aldebaran Resources, at VRIC. There has been some buzz around other company he is CEO, Regulus Resources, in the last few days.

I’ll admit that I haven’t been following the development of Regulus’s asset, Antakori, closely. Nevertheless, I do have faith in John Black, as a CEO who has developed and sold assets several times in LatAm. Here’s my understanding of the situation..

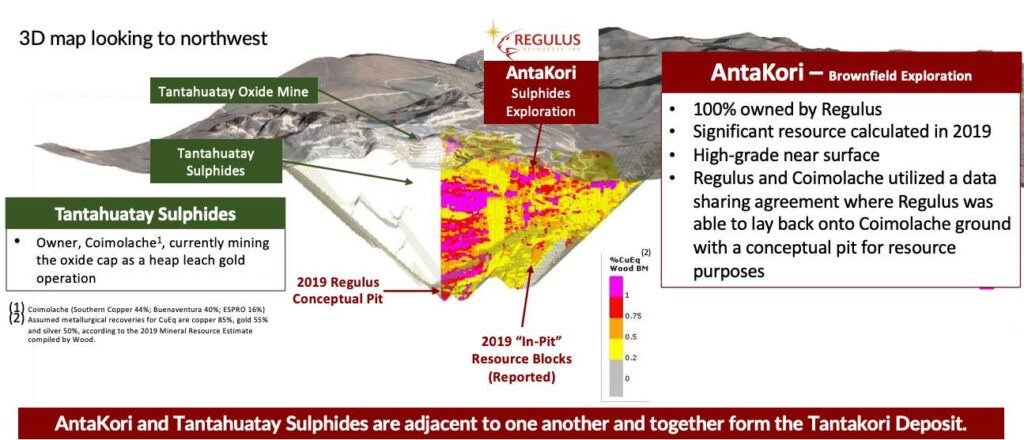

Brief Background

Regulus’s AntaKori project is halved. Half the ground is an operating mine, operated by Buenaventura (BVN on the NYSE), and the other half is Regulus’s property. BVN is currently mining the copper-oxide portion of their Tantahuatay mine.

(Image taken from Regulus March 2024 Corp. Pres, pg 9. )

Reasons for Buzz

- Two nearby mines, the TANTAHUATAY MINE (operated by BVN) and the CERRO CORONA MINE are allegedly running low on ore and will need more ore to operate soon (e.g. two years), making acquisition in the region sensible.

- Tantahuatay is currently mining its copper oxide zone. They will need to develop their copper sulphide zone, which lies below. This will require the same technology REG.V is currently testing with Nuton and would result in synergies if they unified.

- BVN CEO on a Q4 call (see 30:40-minute mark), mentioned that they were talking to BHP about (assumingly an acquisition of) BVN’s Coimolache project, which suggests consolidation of the area would need to happen first.

Comments from John Black from recent videos also indicate that this year they would be in discussing consolidation in the region. John sold the Antares Minerals asset Haquira for 650+ million in 2010 (copying this from the corp. pres). At a MCAP of 113 million today, a similar sale of AntaKori would mean a five bagger. As someone who has grown only more skeptical as I’ve gained some experience in the space, I doubt that would happen for a company that’s not traded much higher than $2 in the past twelve years. Nevertheless, I think it’s a good bet on profit and hoping management can negotiate well.

Other things to like:

- Tight float (similar to Aldebaran)

- Brownfield in an area with a history of mining

Things to dislike:

- Osisko is involved and has an NSR

- They recently reissued all 200k worth of expired options for Senior Vice President Corporate Development at half the strike price (from 1.78 to 0.92)

- High arsenic content (like Aldebaran’s Altar project); the result from Rio Tinto’s Nuton Tech will be out around Q3 I’m guessing, which will inform us how well that works in reducing arsenic levels in copper sulphides.

Copper also seems to be gaining momentum as well and gold definitely is. I took a position.

Disclaimer: This content is for informational purposes only and should not be construed as financial advice. The views expressed are those of the author, who is not liable for any losses or damages arising from any actions taken based on the information provided in this blog. Investing and trading involve risk; you are solely responsible for your decisions.

Pingback: Late July Portfolio Update (Looking Alright) - stocks.threethousand.org

Pingback: 2024 Mining & Resource Sector Portfolio Review - stocks.threethousand.org

Pingback: VRIC 2025 Update - Regulus, Altius, Etc. - stocks.threethousand.org

Pingback: VRIC 2025 Update - Regulus, Altius, Idaho Strategic, & Amerigo - stocks.threethousand.org