It’s been a few months. Here are some updates.

Positions Liquidated for Family Finances

Due to a lull in our household income flow, I decided to take some cash out of the market to have as a buffer for more practical things (food, mortgage). Here are the trades I closed:

- MAG.TO (Mag Silver): Bought at 16.96, sold at 23.57 for a 39% profit. This was a good trade. I had never planned to hold a silver company long-term. It was a bit of a kick on the nuts when MAG was acquired by Pan American Silver about a month after I sold for $25, but still, it was a good trade.

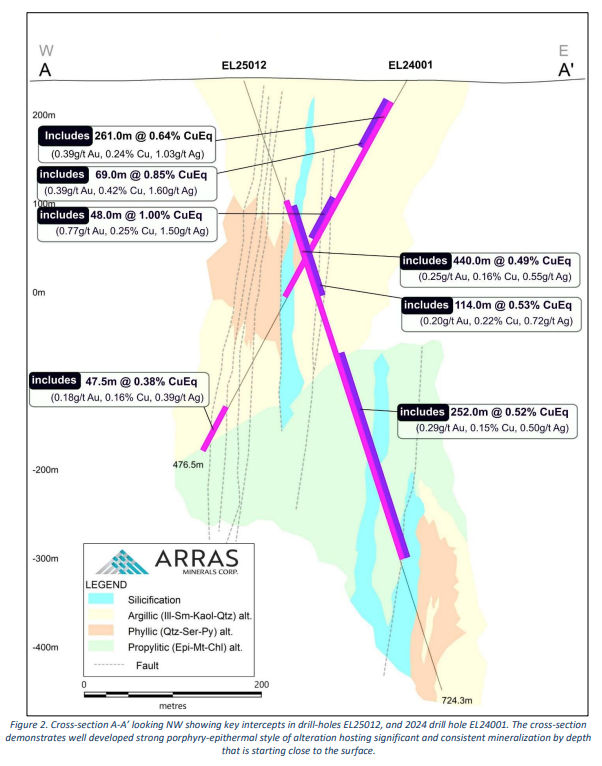

- ARK.V (Arras Minerals): Bought at 0.45c, sold at 0.69c for a 53% gain. This was a company I had wanted to hold longer. It ripped as high as a dollar in July, but has since fallen back to approximately .70c. On the topic of Arras, there have been two recent negative events this week that have made me lose faith in management.

- Firstly, the recent drill results first showed up on Sedar (picked up by CEO.ca) mid-day during trading hours without any formal NR being released. The company then realized its error and released an NR well after the stock’s price had fallen 33% (the results were poor). The company later blamed Access Newswire.

- Secondly, the company is mixing different CuEQ (copper equivalency values) for its drill holes, which boosted its recent headline but is confusing and inconsistent. See thread here. I will not be following the company anymore.

New Positions

I bought some Aecon Group (ARE.TO) for myself and my kid’s RESP. Aecon is a construction and infrastructure company. It first came under my radar from Sultan Ameerali’s posts. Essentially Aecon is a pick-and-shovel play on nuclear buildouts. The stock had been trading much higher before Trump’s liberation day on the theme of increased nuclear adoption. Financially it had been suffering due to legacy turnkey (fixed cost) projects like the Eglington line bleeding cash. The Q2/2025 Fins show a 10.7-billion-dollar order backlog, and an operating profit of $2.3 million (not much but much better than the previous year’s operating loss of $166.3 million). As these legacy turnkey projects come off the books, net income will improve.

ARE.TO pays a 3.7% dividend, has a tight share count (62M ND), and is buying back its own shares. I plan on holding this company for the midterm. I also think the company will do well in this “elbows out” (Canada-focused) environment.

Other Thoughts

- Aurion put out its best drill intercept in a while last week: 4.42 g/t Au over 32.55 m at Kaaresselkä, Risti Property (NR). I continue to like Aurion. The company gives you exploration upside with some downside protection due to the value of its ground right on the border of Rupert Resources proposed open pit. Also the company doesn’t issue the typical DSU/RSU/Options you see diluting other mining companies. The only Sedi reports are Chairman Dave Lotan buying on the open market.

- B2Gold trading at about two-year highs.

- Champion Iron continues to languish. Support seems to be at around $3.6. This would be a safe place to buy if I had more cash and wanted to increase my position. It wouldn’t be a hard range to trade around while waiting for the iron ore market to rebound and for the high-purity iron ore plant to start producing.

- NGEX killing it at ATH and also recently announced a royalty spinout. I should own more shares of NGEX.

- FPX Nickel: Hoping for MOU announcement anytime now…

Good night.

-MB

Disclaimer: This content is for informational purposes only and should not be construed as financial advice. The views expressed are those of the author, who is not liable for any losses or damages arising from any actions taken based on the information provided in this blog. Investing and trading involve risk; you are solely responsible for your decisions.