I skipped MIF (Metals Investors Forum) but attended the Vancouver Resource Investment Conference this year. Below is my attempt to decipher my notes from the interviews I had.

Disclaimer: This post contains forward-looking statements. These statements are based on my memory and rough notes, and as such, they may not accurately represent information about the relevant companies or the views of the interviewees. This content is provided for informational purposes only and is not intended as investment advice.

Regulus Resources (REG.V) Update

Firstly, I attended a Rick Rule talk at 11:20 in which he spoke about the companies at the conference that he owned. Regulus Resources was such a company. He is an owner because of faith in John Black, the CEO, who successfully sold the Antares deposit to First Quantum Minerals for C$650 million. He described John as the opposite of the typical CEO — he is honest about the warts and “what keeps him up at night” about his projects and is more likely to underhype his companies’ developments than oversell them. Rick liked this quality.

At the REG booth John was engaged so I spoke with Ben Cherrington (IR) mostly and Kevin Heather (Chief Geo) a little. Here are a few tidbits:

- The news we’re waiting for is 1) the consolidated MRE for the Tantakori (a play on words for Coimolache’s Tantahuatay side + Regulus’s Antikori side of the deposit) and 2) Nuton results. These two items should be out shortly though no exact timeline was given.

- The MRE will tell us who has what. The ‘Who’ here includes Regulus, obviously, and then Comiolache, which consists of three entities:

- Southern Copper (44%) < a subsidiary of Groupo Mexico and potential acquirer.

- Buenaventura (40%) < a Peru-based producer with a 3.27BMCAP. The impression I got was that BVN doesn’t have the size to be the ultimate buyer of the entire project.

- Espro (16%) < a small Peruvian company too small to be a consolidator.

- Rio Tinto already owns 16% of Regulus. In my opinion, it would be the logical acquirer given the ownership and testing of their Nuton tech. The acquirer could also be a major like BHP, which has its own Nuton-like copper leaching technology.

- John had mentioned recently in an interview that after the MRE, Regulus & Comiolache might put forward a PEA. I asked about the timeline for this but didn’t really get one. The hope from Ben is that a PEA won’t be required because the project will be bought. If a PEA is created, it would present both the base case economics and the Nuton case economics.

- The company has 14M in the bank, which should last two years. Ben does not envision the company will need to raise again before the end is reached.

- Of the existing undeveloped copper projects worldwide, Tantakori represents the easiest to bring into production timewise considering its brownfield setting right beside an existing mine. Plus there’s a need for employment continuity in the region.

- The main difference between the period when Antares was sold (for $650M) is that the market for copper now is much more competitive. There are more majors looking for copper such as those from the Middle East and even Indonesia (see the acquisition of REX Minerals last year.) This should drive a better price.

For the fuller recap of the Regulus story, read my post from last year here. Ultimately I emerged confident in the investment. It truly seems like a matter of when and not if.

Altius Minerals (ALS.TO) Update

I had a short chat with Chad Wells, V-P Business. The story for the next 3-4 months will be all about AngloGold Ashanti’s Silicon Project in Nevada, on which Altius holds a 1.5% NSR. As anyone who’s been following the story knows, there’s been a legal battle about the extent of Altius’s NSR coverage on the region. An arbitrator’s “partial-award” decision was released on Jan 10th. Read it here. I will not rehash it mainly because it’s still indefinite and it’s not entirely clear what sections on the map ultimately encompass Altius’s royalty claims. Chad says this decision was a win for Altius and that full details will be released within 50 days, as the NR states.

Chad pointed to Feb 18th as an important date as that’s when Anglo updates their resource. My notes are a little weak here; not sure if this is for Merlin and/or the Silicon deposit. An updated resource will help crystallize the value of the NSR, which will help ALS shop it around. He admitted that a royalty swap (e.g. for a base metal royalty at Voisey Bay) is a possibility and also that they aren’t ruling out holding onto it if the right offer doesn’t arise.

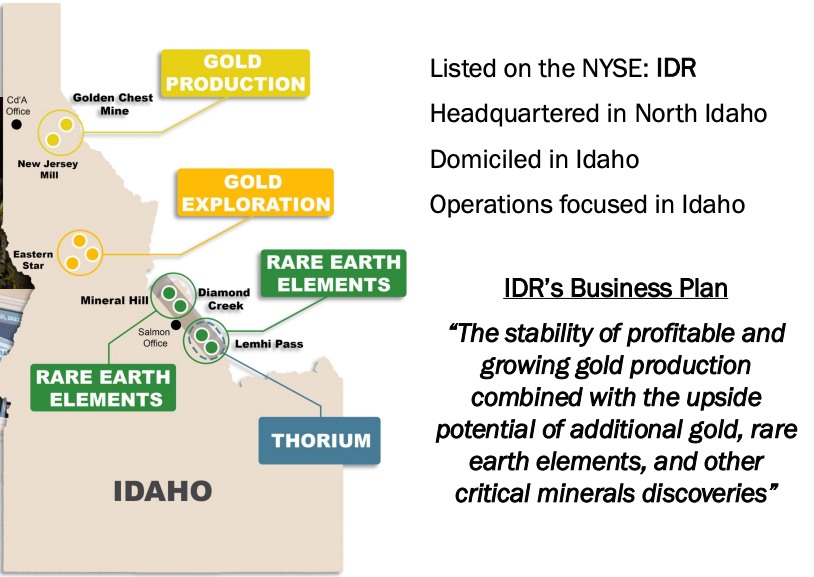

Idaho Strategic Resources (IDR.US)

If you know this stock, you probably heard about it from Ian Cassel (microcap investor with a large following) or perhaps Brandon Beylo (@marketplunger1 on X). The quick recap is that it’s a tightly held stock (12M shares outstanding) run by a down-to-earth kinda guy, John Swallow, who cares about his company and investors. It’s a single-asset gold producer that makes money.

I am more interested in its rare earth elements projects. Here’s a blurb from their website:

Our 100% owned Lemhi Pass, Mineral Hill, and Diamond Creek Projects are located in central Idaho’s REE-Th Belt and recognized as three of the top ten rare earth elements prospects in our country. They are included in the United States’ national strategic inventory and have the potential to serve as a domestic replacement to foreign sources for rare earth elements critical to the U.S.’ decarbonization goals

The idea that you can get the upside of REE exposure, elements that are increasingly being recognized as significant to domestic security, with your downside limited by the cash-flowing Gold Chest mine is a strong selling point. Trump’s America First theme makes REE exposure even more sensible, I figure.

I spoke with the young and capable IR Rep Travis Swallow, the CEO’s son.

First question: What kind of REEs does IDR have? My cursory understanding of REE extraction is that ionic clays are easier to extract.

IDR’s are hard rock in carbonatite. This doesn’t mean they are unextractable of course; no such MET work has been done with their deposits. Travis gave the example of MP Materials’ Mountain Pass Mine as an example of a carbonatite project. I’m familiar with MP Materials’ story; I was a little turned off to learn they were created via a SPAC in 2021.

Here’s IDR’s map that we were looking at.

For more details of IDR’s three REE deposits (Mineral Hill, Diamond Creek, and Lemhi Pass), see page eleven of their corporate pres (recent one). The upcoming rare earth plans for IDR’s REE are a trenching program in the summer and possible geophysics at Lemhi Pass. The company’s gold-related plans are as follows:

- 30 holes at Gold Chest, with results probably in 1.5 months. This drilling I believe is part of their SK-1300 requirements; including infilling and some step-outs (if I remember correctly).

- Exploration drilling on their Eastern Star property from April to September. This deposit has been trenched but never drilled properly as it was covered by trees until recent logging by a TImber company.

Overall, this is a company I will continue to monitor and look for an opportunistic entry. I’m not dying for more gold exposure and the rare earth’s progress is moving slowly though work is being done.

Amerigo Resources (ARG.TO) aka the Copper Factory

I first heard of this company at VRIC last year from a recommendation at a public talk given by Nicole Adshead-Bell. The controversial Mark Turner is also a fan, a man who’s hard to please. Also when talking with Ben Cherrington from Regulus earlier today, this was a pick of his. If you watch an Amerigo presentation, what’s obvious is the competence of the CEO Aurora Davidson, who I was able to talk to.

This was a brief talk; I was getting tired and frankly Amerigo’s story isn’t one that requires detective-like questioning. ARG makes money by extracting copper and moly from Codelco’s tailings. Codelco is Chile’s national copper company. The tailings come from the El Teniente mine, which has been operating since 1905 and has a LOM until 2082. Amerigo processes both old and new tailing ponds, and there is virtually an unlimited amount. The company pays a fat quarterly dividend yield of 7.7%, and there’s an option of a bonus performance divvy in favorable market conditions.

I asked about the risks. Aurora said weather, e.g. rain or earthquakes. They made water efficiency improvements recently to mitigate water supply risks.

She mentioned the company will by debt-free by the end of this year and the company has completed major upgrades to move it from 35-40 to 60 million pds/year.

This isn’t really a growth stock; it’s a bet on strong copper prices. Ultimately, ARG is a pragmatic investment (dividend and copper exposure) and it also is a green play, given they are extracting copper from tailings waste. I’ve been following it for a year and missed out on a 30% run-up in share price and dividends. With that said, I put my money into Regulus, which has more than doubled. When Regulus is acquired, I will look to Amerigo as a more conservative play.

There are likely some inaccuracies above and there’s definitely a lack of precision. Excuse my notes. Ultimately, I write these summaries for myself to help me reflect. They should not be considered accurate. Overall, it was a successful afternoon. I was able to ask some insiders about the CEO of company I’m considering taking a punt on; I built a connection, and I ran into a few acquaintances in the space and got to hear their portfolio updates.

That’s a wrap for VRIC 2025.

Disclaimer: This content is for informational purposes only and should not be construed as financial advice. The views expressed are those of the author, who is not liable for any losses or damages arising from any actions taken based on the information provided in this blog. Investing and trading involve risk; you are solely responsible for your decisions.