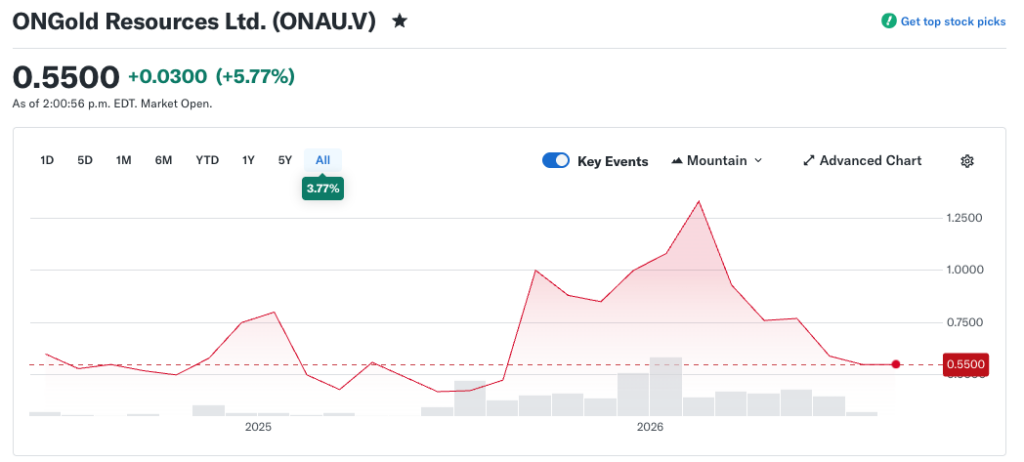

Though I continue to follow the market and my watchlists, I hadn’t made any buys in a while because my industry (teaching) is in a downturn. I made an exception last week, however, with my first purchase of shares in ONGold Resources.

Overview

- Ticker: ONAU.V

- Shares Out: 73.96M (non-diluted)

- Market Cap: $40M

The company and its assets were spun out of Northern Superior in 2024, prior to IAMGOLD’s acquisition of Northern Superior. The current CEO, Kyle Stanfield, was selected by Michael Gentile, a key strategic investor.

The company has two projects with notable activity.

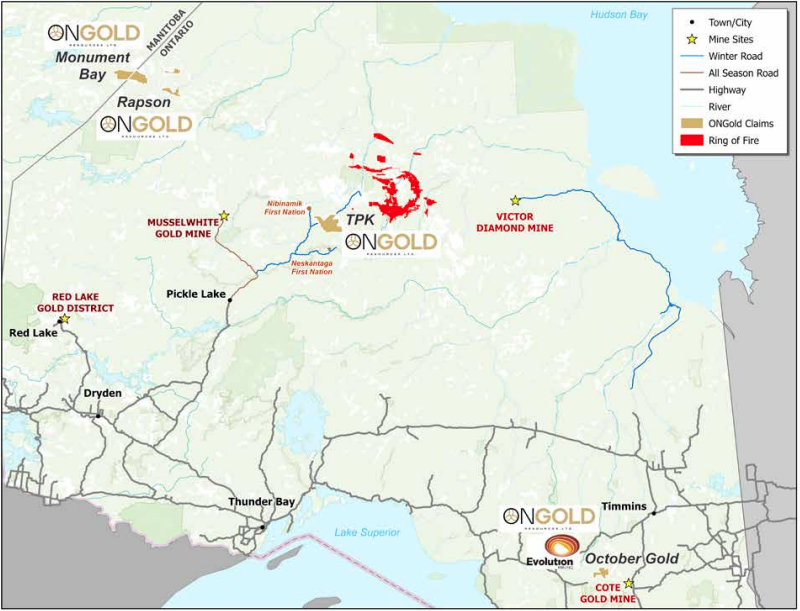

Monument Bay (MB) Gold & Tungsten Project, North East Manitoba

The project has had seven previous owners since 1987. It has a historic 3 million-ounce resource (M&I and inferred)) at 1.15 g/t and was purchased by ONGold from Agnico Eagle for $250,000 cash plus shares in ONGold, with Agnico retaining an equity position in the company. Monument Bay is accessible by aircraft and then ice road in winter.

ONGold is currently reassaying historical core to release an updated MRE in fall 2026 (soon), which will include tungsten and a number of historical holes that were not included in the previous estimate. This will be a catalyst.

The Tungsten (W03) Kicker

In 2011, a master’s student was the first to notice that the core contained tungsten, which had not been assayed for by previous owners Beema Gold. According to this Northern Miner article, operator Mega Precious Metals claimed in 2014 that MB had 248,000mtu (metric tungsten units) or 3,430 tonnes, which is not very large (reference: MacTung has approximately 374,000 tonnes).

A qualified professional, however, will do the estimate for us in the updated MRE. The growth in tonnage should strengthen the AuEQ calculation, improving the project’s economics.

The CEO noted that Monument Bay will continue to primarily be a gold project, but more importantly, the additional critical mineral angle could open doors for development/funding. ONGold was already given $300,000 in funding from the Manitoba government, which has approved Monument Bay as a Manitoba Mineral Development Fund-approved project.

Ti-Pi-Haa-Kaa-Ning (TPK) Gold & Copper Project, Ontario

Allegedly, Gentile became interested in Northern Superior because of the TPK project. The project holds the title of “one of the largest unsourced gold till anomalies in North America.” From what I can infer, the project has not had drilling since 2012.

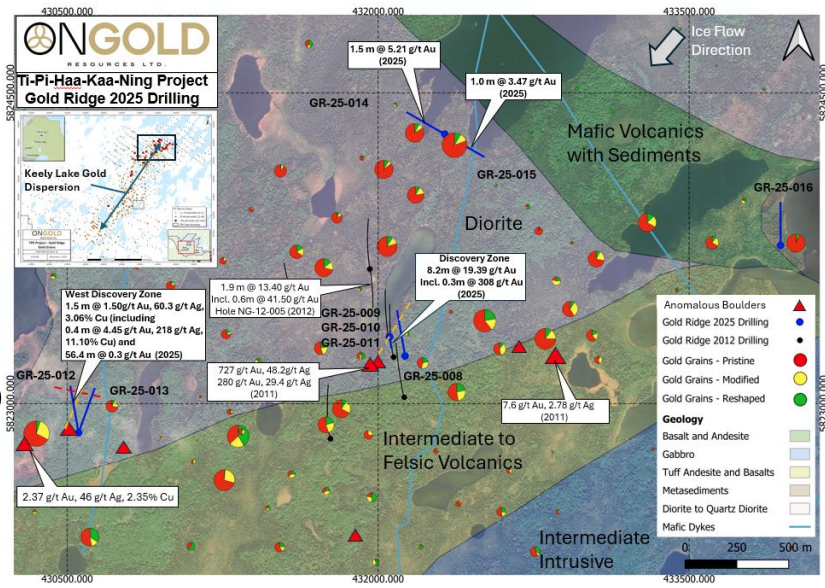

In 2025, ONGold received its exploration agreement from the local Nibinamik First Nation in September, 2025. Fall 2025 drilling identified high grades at the Gold Ridge area, including 19.39 g/t gold over a core length of 8.2 metres. The project has blue-sky exploration potential, and better infrastructure, accessible by a winter road off an all-season road leading from the nearby Musselwhite Gold Mine.

Here’s my summary.

Reasons I bought OnGold:

- Upcoming Catalyst: the MB MRE (fall, 2026)

- Strategic Backing: Michael Gentile (6%) and Agnico Eagle (12%) are existing shareholders.

- Valuation Backstop: The 3M+ oz Monument Bay is much more buildable at $4,000+/oz gold. I don’t buy pure exploration plays, so the project provides a valuation backstop.

- Strategic Kicker: Though Monument Bay won’t be a MacTung, a strategic metal strengthens the developmentability of a precious metals project.

- Clean Structure: ~74M shares

Potential Issues

Monument Bay

- Water: Some of the deposit is underwater (about 4m), and therefore a diversion of the water would be required. Anytime water is touched, governmental and community consent become crucial.

I spoke to the CEO on this point and this did not seem like a major concern at this time. The relevant First Nation here is the Red Sucker Lake First Nation (RSLFN). Kyle is pleased with the progress they’ve made in developing their relationship, which has improved from the AEM days. The RSLFN did provide consent for ONGold to resume exploration in February of 2025. He believes they’ll be willing to work together as the project advances.

- Infrastructure: The project will need a road and powerline is 50km away. In this sense, it’s not a very Gentile-like project. He tends to favor infrastructure-friendly projects near existing mines.

- Encumbrances:

- Franco-Nevada has a 2% NSR, which actually increases to 3% after 1M oz are produced (in certain portions of the project).

- Triple Flag has a 1.5% NSR on some areas of the project.

Hopefully a portion of these can be bought back as the project advances.

What’s Next For The Company

The company currently has $1.5M in cash, but they are fully funded for their MB and TPK programs.

- Monument Bay: The updated MRE will be released in the fall.

- TPK: The company is currently spending 1 million on additional geophysics and prospecting at TPK as part of its Phase 1. Drilling will commence in the fall.

Conclusion

ONGold is the eighth owner of Monument Bay since 1987. The hopes here are threefold: 1) that ONGold is the right team, 2) the updated resource estimate will add size, better economics, and strategic importance, and 3) that a $4,000 POG is the right environment to move it forward.

Overall, I see a company trading at a measly $40M market cap with a valuation backstopped by a 3M oz deposit that’s set to grow in a significant news release in a few months.

Further Reading:

- X post by @torchincapital on ONAU.V https://x.com/torchincapital/status/2014747913721688134

- X post by @YellowLabLife on tungsten at MB https://x.com/YellowLabLife/status/2019068829624594477

- X post by @YellowLabLife on history of MB https://x.com/YellowLabLife/status/2003852057590079684

Disclaimer: This content is for informational purposes only and should not be construed as financial advice. The views expressed are those of the author, who is not liable for any losses or damages arising from any actions taken based on the information provided in this blog. Investing and trading involve risk; you are solely responsible for your decisions.